Unlocking Cost Efficiency: A Comprehensive Guide to Activity-Based Costing for Internal Subsidiaries

In today's dynamic business landscape, organizations are constantly seeking innovative ways to optimize their cost structures and enhance decision-making. Activity-based costing (ABC) has emerged as a powerful tool for internal subsidiaries to achieve these objectives. This comprehensive guide will delve into the intricacies of implementing ABC for internal subsidiaries, empowering businesses to unlock cost efficiency and drive organizational excellence.

4.5 out of 5

| Language | : | English |

| File size | : | 2186 KB |

| Text-to-Speech | : | Enabled |

| Enhanced typesetting | : | Enabled |

| Word Wise | : | Enabled |

| Print length | : | 156 pages |

| Screen Reader | : | Supported |

What is Activity-Based Costing (ABC)?

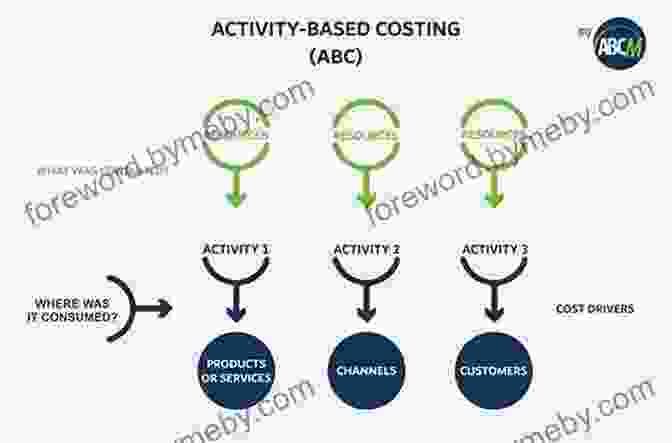

Activity-based costing (ABC) is a cost accounting method that allocates costs to activities and then to products or services based on the resources consumed. Unlike traditional cost allocation methods, which rely on volume-based drivers such as labor hours or machine hours, ABC considers the actual activities performed to produce a product or service. This approach provides a more accurate and granular understanding of cost behavior.

Benefits of Implementing ABC for Internal Subsidiaries

- Improved Cost Allocation: ABC helps internal subsidiaries allocate costs more accurately to activities and products, leading to a better understanding of true cost drivers.

- Enhanced Decision-Making: With a clear understanding of cost drivers, internal subsidiaries can make more informed decisions about product pricing, resource allocation, and process improvement.

- Increased Efficiency: By identifying non-value-added activities, internal subsidiaries can streamline operations and reduce unnecessary costs.

- Improved Communication: ABC provides a common language for discussing costs, fostering collaboration and alignment throughout the organization.

- Enhanced Competitive Advantage: By optimizing cost structures and improving decision-making, internal subsidiaries can gain a competitive edge in the marketplace.

Implementation of ABC for Internal Subsidiaries

Implementing ABC for internal subsidiaries involves a systematic process. Here are the key steps:

- Define Activities: Identify the activities performed within the internal subsidiary and group them into logical categories.

- Identify Cost Drivers: Determine the factors that drive the cost of each activity, such as labor hours, material usage, or overhead expenses.

- Collect Activity Data: Gather data on the resources consumed by each activity, including labor costs, materials, and overhead allocations.

- Calculate Activity Rates: Divide the total cost of each activity by the corresponding cost driver to determine the activity rate.

- Allocate Costs to Products or Services: Assign costs to products or services based on the activities performed to produce them.

- Analyze and Interpret Results: Review the cost allocation results and identify areas for cost reduction and process improvement.

Challenges of Implementing ABC

While ABC offers significant benefits, its implementation can come with challenges. Some of the common obstacles include:

- Data Collection: Gathering accurate activity data can be time-consuming and resource-intensive.

- Complexity: ABC models can be complex to develop and maintain, especially for large organizations with numerous activities.

- Subjectivity: The identification of activities and cost drivers can involve subjective judgments.

- Organizational Resistance: Implementing ABC may require significant organizational change, which can encounter resistance from employees.

Overcoming Implementation Challenges

To overcome the challenges of ABC implementation, internal subsidiaries can adopt the following strategies:

- Phased Implementation: Implement ABC in a gradual and manageable manner, starting with a pilot project or a specific business unit.

- Employee Involvement: Engage employees throughout the implementation process to gain their buy-in and expertise.

- Technology Support: Leverage technology solutions to automate data collection and analysis, reducing the complexity and time required.

- Continuous Improvement: Regularly review and refine the ABC model to ensure its accuracy and relevance.

Implementing activity-based costing (ABC) for internal subsidiaries offers a transformative approach to cost allocation and decision-making. By accurately identifying cost drivers, allocating costs more precisely, and enhancing communication, internal subsidiaries can unlock cost efficiency, improve operations, and drive organizational excellence. Overcoming the implementation challenges requires a well-planned approach, employee involvement, technology support, and a commitment to continuous improvement. Embracing ABC empowers internal subsidiaries to become more competitive, agile, and responsive to the ever-changing business landscape.

4.5 out of 5

| Language | : | English |

| File size | : | 2186 KB |

| Text-to-Speech | : | Enabled |

| Enhanced typesetting | : | Enabled |

| Word Wise | : | Enabled |

| Print length | : | 156 pages |

| Screen Reader | : | Supported |

Do you want to contribute by writing guest posts on this blog?

Please contact us and send us a resume of previous articles that you have written.

Book

Book Novel

Novel Page

Page Chapter

Chapter Text

Text Story

Story Genre

Genre Reader

Reader Library

Library Paperback

Paperback E-book

E-book Magazine

Magazine Newspaper

Newspaper Paragraph

Paragraph Sentence

Sentence Bookmark

Bookmark Shelf

Shelf Glossary

Glossary Bibliography

Bibliography Foreword

Foreword Preface

Preface Synopsis

Synopsis Annotation

Annotation Footnote

Footnote Manuscript

Manuscript Scroll

Scroll Codex

Codex Tome

Tome Bestseller

Bestseller Classics

Classics Library card

Library card Narrative

Narrative Biography

Biography Autobiography

Autobiography Memoir

Memoir Reference

Reference Encyclopedia

Encyclopedia Felix Scheinberger

Felix Scheinberger Executivegrowth Summaries

Executivegrowth Summaries Frederick Kaufman

Frederick Kaufman Jonathan White

Jonathan White Ethan De Seife

Ethan De Seife Janna Herron

Janna Herron Fred Mcallen

Fred Mcallen Frank Holland

Frank Holland Flor M Salvador

Flor M Salvador Fred J Young

Fred J Young Jackie Faasisila

Jackie Faasisila Fred Nadis

Fred Nadis Jesse Braun

Jesse Braun Kenneth P Price Ph D

Kenneth P Price Ph D Isabel Toledo

Isabel Toledo Francisco Martin Rayo

Francisco Martin Rayo Frederick D Patterson

Frederick D Patterson Frank Nappi

Frank Nappi Lauren Oliver

Lauren Oliver Firefighter Now

Firefighter Now

Light bulbAdvertise smarter! Our strategic ad space ensures maximum exposure. Reserve your spot today!

Samuel WardSpace Relocation and the Politics of Identity in Global Cairo: A Journey into...

Samuel WardSpace Relocation and the Politics of Identity in Global Cairo: A Journey into...

Philip BellFollow ·14.6k

Philip BellFollow ·14.6k Terence NelsonFollow ·8.2k

Terence NelsonFollow ·8.2k James JoyceFollow ·16.1k

James JoyceFollow ·16.1k Marvin HayesFollow ·5.2k

Marvin HayesFollow ·5.2k Darren BlairFollow ·3.3k

Darren BlairFollow ·3.3k Nathan ReedFollow ·10.6k

Nathan ReedFollow ·10.6k Alfred RossFollow ·7.7k

Alfred RossFollow ·7.7k Melvin BlairFollow ·2.4k

Melvin BlairFollow ·2.4k

Al Foster

Al FosterDive into the Enchanting World of Manatees: An...

Unveiling the Secrets of the Gentle...

Isaac Mitchell

Isaac MitchellThe Farm Reggie and Friends: US Version - A Captivating...

A Heartwarming Tale that Embraces...

Esteban Cox

Esteban CoxThe Interior Design Handbook: Your Comprehensive Guide to...

Are you ready to...

William Wordsworth

William WordsworthFall Head Over Heels for "Esio Trot" by Roald Dahl: A...

Prepare to be charmed, amused, and utterly...

Caleb Carter

Caleb CarterBlack Clover Vol Light Frida Ramstedt: A Thrilling...

Prepare to be spellbound by...

Richard Simmons

Richard SimmonsFantastic Mr. Fox: A Literary Adventure That Captivates...

In the realm...

4.5 out of 5

| Language | : | English |

| File size | : | 2186 KB |

| Text-to-Speech | : | Enabled |

| Enhanced typesetting | : | Enabled |

| Word Wise | : | Enabled |

| Print length | : | 156 pages |

| Screen Reader | : | Supported |